Honest reading. No selling.

Short reads on the messy reality of personal finance. State-level payday rules, APR math without the brain fog, earned wage access, repayment strategies, and the small habits that make a tight month less tight.

Pawn Shop or Online Loan? The Honest Tradeoff Nobody Explains

Pawn risks your stuff. Online installment risks your credit. They are not interchangeable. Here is the real tradeoff before you walk in or click Apply.

Thinking About Consolidating Your Loans? Run This Quick Test First

For small balances, consolidation can quietly cost more even at a lower rate. A two-line math test that tells you whether to refi, consolidate, or just keep paying.

Is 'Pay in 4' a Loan? The Honest Answer Before You Tap That Button

BNPL feels like a checkout button, but Pay in 4 is a six-week loan. Here is when it rescues a tight week, and when it quietly stacks up against you.

Debt Collectors Will Not Stop Calling? Here Is How to Make Them Pay

Every illegal call has a price tag of $500 to $1,500. Here is how to log the evidence, file the complaint, and stop the harassment without an attorney.

Payday Loans Banned in Your State? Here Is What Is Actually Legal

If you live in one of the 18 payday-restrictive states, your Google results are mostly unlicensed lenders dodging the rules. Here are the legal paths in order of cost.

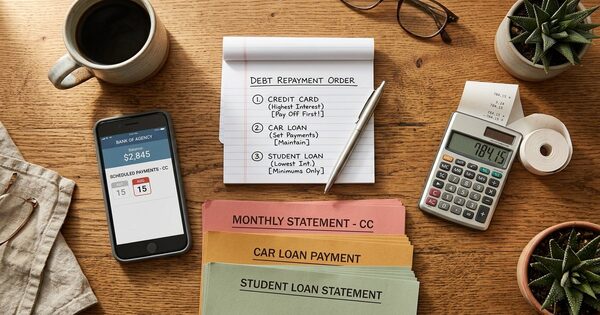

Behind on Three Loans? Here Is Which One to Pay First

Snowball, avalanche, or just whichever lender is yelling loudest? A practical priority order for a payday, installment, credit card, and BNPL stack under $5,000.

Behind on Rent? The Eviction-Day Playbook (Where the Help Actually Is)

Most rental-assistance articles still link to programs that closed in 2025. Here is the real 2026 path: who to call tonight, what to apply for this week, when a loan helps.

The 28% Loan Most Payday Borrowers Have Never Heard Of

Federally regulated credit unions can offer a Payday Alternative Loan capped at 28% APR with a $20 fee. Here is how to find one and what to do when your credit union does not offer them.

How to Save Your First $1,000 (When You Are Living Paycheck to Paycheck)

Skip the "six months of expenses" cliche. A real plan that starts at $250 in 12 weeks, hits $1,000, and explains why crossing that line changes everything else.