Debt Repayment Order for Small-Dollar Borrowers: A 3-Step Priority System

Quick answer: Snowball and avalanche were written for $40,000 student-loan stacks. For a $3,200 mix of payday, installment, BNPL, and credit card debt, the right order is: (1) pay whatever triggers an NSF or rollover in the next 7 days, (2) attack the highest APR with whatever is left, (3) clear the smallest balances last for mental load. Cash flow first, APR second, ego third.

The standard "snowball vs. avalanche" article was written for someone with $40,000 in student loans, two credit cards at 22%, and a car payment. That is not your stack. Your stack is a $400 payday loan due Friday, an $1,800 installment loan at 89% APR, a $600 credit card at 26%, and a $400 buy-now-pay-later balance spread across two apps. The interest rates are not "high vs. higher." They are "29% vs. 400%." When the spread is that wide, the method you pick matters less than the order you pay them in.

Here is the version that fits a Quick5k-shaped debt stack: a three-step priority order calibrated for borrowers juggling two to five small balances under $5,000 total, with a worked example on a $3,200 stack and the specific questions to ask before you send the next payment.

The 60-Second Triage

Before you think about APR, balance, or payoff strategy, answer one question: what is being pulled in the next seven days?

Small-dollar borrowers do not lose ground because they pick the wrong long-term strategy. They lose ground because an ACH pull empties the checking account, the rent payment bounces, the bank charges a $30 NSF fee, and a second pull is reattempted three days later for another $30 fee. The CFPB's research on bank junk fees put the average NSF charge at $26 to $35 per item in 2024. Two reattempted ACH pulls on a payday loan can put $70 in fees on top of the loan you cannot pay.

Pull up your checking account. List every debit scheduled in the next seven days. The first payment you make is the one that prevents the cash-flow cascade, even if it is not the loan with the highest APR. If overdraft fees keep stacking, our checking account setup guide shows how to switch to a no-overdraft account before another cycle hits.

Sort Your Debts by Three Numbers, Not One

For every balance you have, write down three things:

- Current balance

- APR (or the equivalent fee structure for payday and BNPL)

- Next due date and how it gets paid (auto-debit, manual, scheduled withdrawal)

That third column is the one most advice articles skip. A 26% credit card that you pay manually next month is a slow-moving problem. A 400% payday loan with an auto-debit Friday morning is an emergency that has already started.

Why Snowball Alone Fails Small-Dollar Borrowers

The snowball method (pay the smallest balance first to build momentum) has a real psychological track record. The Kellogg School research that gave snowball its credibility found borrowers stuck with payoff plans longer when they hit early wins. Fine. But that research was run on debt stacks where the smallest balance was usually also a moderate-rate balance, like a $400 store card at 24%.

In a small-dollar stack, the smallest balance is often the most expensive one. A $300 payday loan at 391% APR will cost you roughly $45 in fees every two weeks until it is paid. A $1,200 installment loan at 89% APR costs you about $88 a month. Paying off the $300 payday loan first is the right call, but not because it is small. It is the right call because it is the most expensive dollar of debt you are holding, by a wide margin.

Snowball gets the order right by accident here. The trouble is when it gets the order wrong, which it does as soon as the smallest balance is the cheapest. The $400 BNPL balance might be 0% if paid on time. Paying that off first because it is small means leaving the 391% payday loan to keep generating fees. That is a math mistake dressed as a motivational win.

Why Avalanche Alone Fails Too

Avalanche (pay highest APR first) gets the math right. The problem is that pure avalanche assumes you can make all minimum payments while you direct extra cash to the highest-APR balance. For small-dollar borrowers, "minimum payments" do not really exist. A payday loan is due in full on a specific date. Skip it, and the loan does not roll into a manageable minimum. It rolls over with a new fee, or the lender reattempts the ACH, or it goes to collections.

Pure avalanche on a payday loan stack does not work. The payday loan demands the entire balance every two weeks, whether the APR math says it is the priority or not.

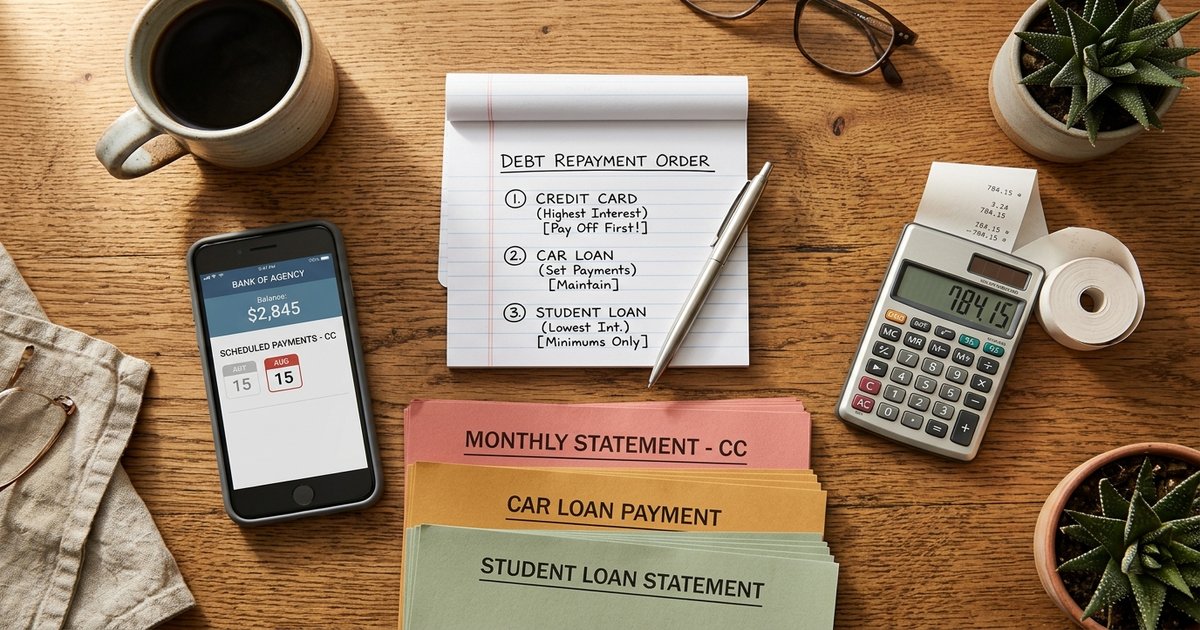

The Three-Step Priority Order

Here is the hybrid that fits a small-dollar stack.

Step 1: Stabilize Cash Flow

Pay whatever is going to trigger an NSF cascade or an immediate cash-flow event in the next seven days. This is almost always the payday loan with a Friday auto-debit, or a rent payment that is already late. It is not about APR. It is about preventing a $70 NSF stack on top of a $400 loan.

If you have a payday loan due Friday and you cannot cover both the loan and your other essential bills, call the lender before the ACH pull. Many state-licensed payday lenders are required by state law to offer an extended payment plan if you ask before you default. The CFPB's research found that 80 percent of payday loans get rolled over within 14 days, which is the worst outcome. An extended payment plan, where available, is structurally better than a rollover.

Step 2: Kill the Highest APR With Whatever Is Left

Once your cash flow is stable for the week, every extra dollar goes to the highest-APR balance. For most Quick5k-shaped stacks, that is the payday loan or a triple-digit-APR installment loan, not the credit card.

This is where the math starts working for you. Federal Reserve data from July 2024 shows the median small-dollar loan balance is $507 with a median monthly payment of $89. Subprime borrowers hold roughly 70 percent of those balances. The dollar you put toward a 391% APR loan saves you about ten times what the same dollar saves you against a 26% credit card. Treat it that way.

Step 3: Pick Up the Smallest Balances to Clear Mental Load

Once the highest-APR balance is gone, your stack is shorter and the math is less brutal. Now snowball logic starts to earn its keep. Pay off the smallest remaining balance next, then the next smallest, then the next. The early wins keep you focused, and at this point the APR spread between your remaining balances is narrow enough that the avalanche math is a rounding difference.

The order in plain English: cash flow first, APR second, ego third.

Worked Example: $3,200 Across Four Places

Take a borrower with the following stack:

- $400 payday loan, 391% APR, auto-debit Friday

- $1,800 installment loan (OppLoans-style), 89% APR, $145 monthly payment due in 12 days

- $600 credit card balance, 26% APR, $25 minimum due in 18 days

- $400 BNPL (split: $200 Klarna, $200 Afterpay), 0% if paid on time, next installments in 4 and 9 days

Suppose you have $620 in your checking account today and a paycheck of $1,150 coming next Friday.

Day 0 to day 7: The payday loan is the immediate cash-flow event. If you let it auto-debit and your account empties, the BNPL installment due in four days will bounce. Pay the $400 payday loan now. Pay the $50 Klarna installment due in four days from what is left ($170 after the payday payoff, assuming no other immediate bills). You still have a $50 BNPL payment due in nine days that you will cover from the next paycheck.

Paycheck Friday: $1,150 lands. Set aside whatever your minimum living costs are for the next two weeks. From whatever remains, the highest-APR debt left is the 89% installment loan. The credit card at 26% looks scary, but it is the cheapest debt left. Make the $145 monthly payment on the installment loan and put as much extra as you can on principal.

Following weeks: Continue routing every extra dollar to the 89% installment loan until it is gone. Make the $25 minimum on the credit card and the small BNPL installments as scheduled. Once the installment loan is paid, switch to the credit card and the remaining BNPL.

The structure: prevent the NSF cascade, then attack the highest APR until the dangerous part of your stack is gone, then clean up the rest.

Call the Lender Before You Miss a Payment

One detail that punches above its weight: call the lender before you miss, not after. Many lenders have hardship programs they do not advertise. The CFPB has documented that state-licensed payday lenders in a number of states are required to offer extended payment plans on request, and most installment lenders have an internal "hardship deferral" option for borrowers who reach out proactively. Once you miss a payment, your leverage drops. Once it goes to collections, your leverage is gone. Our missed payment 12-month timeline spells out exactly what happens at each stage.

Specific phrasing that works on the phone: "I want to pay this loan back. I am asking what options you have for borrowers who need to adjust the payment schedule before they fall behind." That sentence triggers a different routing path inside most lenders' call centers than "I cannot pay."

When Consolidation Makes the Math Work, and When It Does Not

For balances under $5,000, consolidation is a maybe, not a default. The new loan has to cover what you owe, the APR has to be meaningfully lower than the blended APR of your current stack, and the origination fee has to be small enough that it does not eat the savings. The math test: the new loan's total of payments has to be lower than the total of payments you would make under your current stack on your current trajectory. Our refinancing guide walks through the total-of-payments check in detail.

Credit union Payday Alternative Loans (PALs) cap APR at 28% with a $20 max application fee, which is a strong fit for replacing a payday loan if you can join a credit union. A standard personal loan from a bank, online lender, or lending-partner network can work for borrowers with credit profiles strong enough to get a sub-30% APR, but the origination fee (often 1% to 10%) matters as much as the rate.

If you are looking at a $3,200 stack and a consolidation lender quotes 36% APR with a 6% origination fee on a 36-month term, run the total-of-payments math before you sign. Sometimes the answer is "pay the original stack down faster instead."

When to Stop DIY-ing and Call a Nonprofit Credit Counselor

Three signals that your stack has outgrown the priority-order playbook:

- You are taking new short-term loans every cycle to cover the previous cycle's loans.

- Your total minimum monthly debt payments exceed 50 percent of your take-home pay.

- You have an account in collections or a wage garnishment notice.

If any of those describe your situation, a nonprofit credit counselor from an NFCC-affiliated agency can pull your full picture, negotiate with creditors, and sometimes set up a Debt Management Plan that reduces APR on enrolled accounts to 6 to 10 percent. The intake counseling is free at NFCC member agencies. The DMP itself has a small monthly fee but is the legitimate version of what for-profit "debt relief" companies advertise at much higher cost.

The borrowers who get out of a small-dollar stack are not the ones who found the perfect method. They are the ones who stopped letting the next ACH pull dictate the order, and started paying in the sequence that protects cash flow first and kills the most expensive debt second.

Frequently Asked Questions

If your payday loan is on auto-debit and will trigger an NSF cascade, pay the payday loan first to protect your checking account. After that, the math is clear: at 391% APR, the payday loan is roughly 15 times more expensive per dollar than a 26% credit card. The credit card minimum payment can usually be made for $25 to keep the account current while you direct the rest of your cash at the payday loan.

It depends on the provider. Affirm began furnishing all of its products, including Pay in 4, to Experian in April 2025, so on-time payment of an Affirm balance can help. Other providers report inconsistently or not at all. Missed BNPL payments sent to collections will hurt your score regardless of whether the original plan was reported. The score upside of paying BNPL off early is usually small. The cash-flow upside (eliminating bi-weekly auto-debits) is larger.

For a credit card or an installment loan, paying the minimum and ignoring one balance means late fees, then a 30-day late mark on your credit report, then potentially collections after 90 to 180 days. For a payday loan, "minimum" does not really exist: the full balance is due on the due date, and skipping it triggers rollover fees, reattempted ACH pulls, NSF fees, or referral to collections. Sliding a payday loan is structurally more expensive than sliding any other debt type.

Often, yes. Most state-licensed payday lenders are required by state law to offer an extended payment plan on request, and most installment lenders have an internal hardship program. The leverage is in calling before you fall behind. After a missed payment, the conversation shifts from "let's restructure" to "let's settle," and the terms get worse.

Sometimes. The test is total-of-payments, not APR or monthly payment alone. If a consolidation loan replaces a 391% payday balance and a 89% installment balance with one 28% PAL or a 30% personal loan, the savings can be significant. If it adds a 6% origination fee and stretches the term from 12 to 36 months at 35% APR, the total cost can rise even though the monthly payment drops. Run the math before signing.

If you are borrowing to make payments on previous borrowing, if total minimum payments exceed half your take-home pay, or if any account has gone to collections, that is the threshold. Free intake counseling is available through NFCC member agencies. It is not the same as for-profit debt relief, and it does not require you to stop paying creditors first (which is a red flag any time you hear it).