Payday Loans Banned in Your State? Here Are the Legal Options

Eighteen states plus the District of Columbia have effectively shut down payday lending, and yet the search results in those states still light up with "instant approval" ads at midnight. The legal options for a borrower in one of those jurisdictions actually exist, they are just quieter: a credit union Payday Alternative Loan capped at 28 percent APR, a state-licensed installment loan from $500 to $5,000, registered earned wage access through an employer, a workplace hardship program, a 0 percent intro credit card, BNPL for a specific essential bill, and at the bottom of the list, a pawn loan or money from family. The lender at the top of the Google ad is almost never on that list.

A woman in Queens types "payday loan near me" into Google at 11 p.m. on a Sunday. Her rent is short by $800 and the landlord wants it Tuesday. The first three results promise instant approval. One says "available in all 50 states." Another says "tribal lender, state laws do not apply." A third looks like a legitimate storefront chain. She fills out the form on the third one and gets approved for $1,000 at what the disclosure later reveals is an effective rate north of 300 percent.

Here is the part nobody told her: payday lending is illegal in New York. Has been for years. The New York Department of Financial Services treats non-bank consumer loans above 25 percent annual interest as criminal usury under General Obligations Law section 5-501. The lender she just signed with is almost certainly not licensed to operate in her state, and depending on how the loan is structured, she may not legally owe anything beyond principal.

That gap, the one between what Google shows you and what your state actually permits, is where this article lives. If you are in a payday-ban state and need $500 to $2,000 in a hurry, the legal options exist. They are just quieter than the illegal ones.

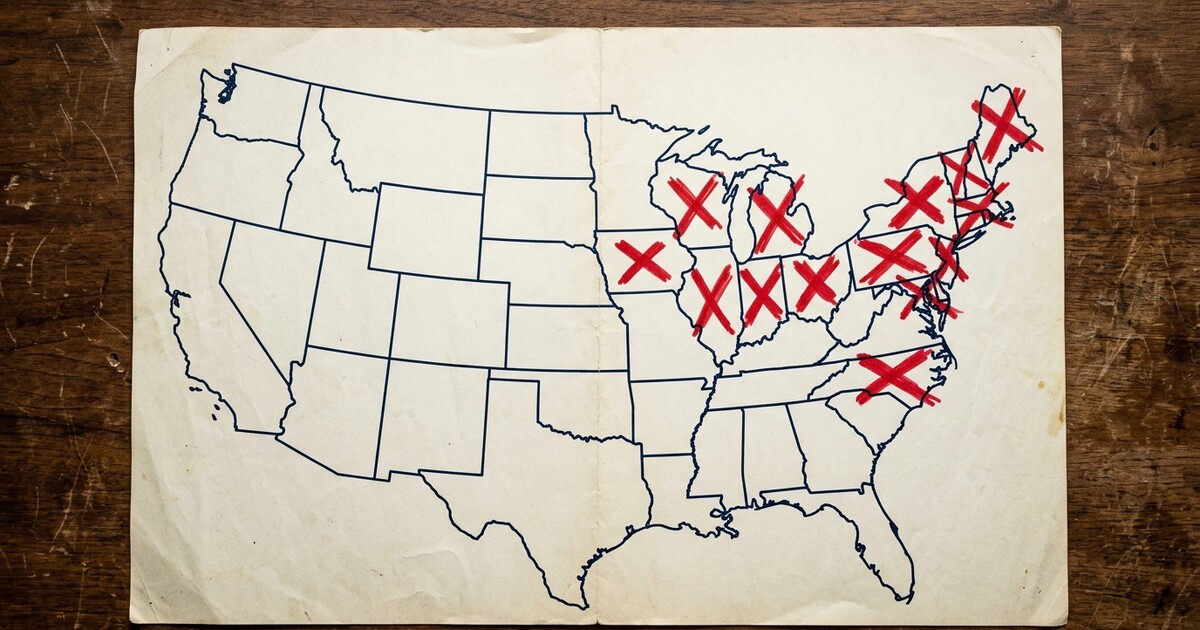

The 18 States Where Payday Lending Is Effectively Banned

According to the Pew Charitable Trusts and the National Conference of State Legislatures, 18 states plus the District of Columbia either prohibit payday lending outright or cap rates low enough that storefront payday operators cannot run a profitable business there. The list: Arizona, Arkansas, Connecticut, Georgia, Illinois, Maryland, Massachusetts, Montana, Nebraska, New Hampshire, New Jersey, New Mexico, New York, North Carolina, Pennsylvania, South Dakota, Vermont, and West Virginia.

The rate caps in those states are not symbolic. New Jersey holds non-bank consumer loans to 30 percent under its Consumer Finance Licensing Act. Connecticut sets the ceiling at 36 percent APR on small consumer loans and bars check cashers from offering payday-style products under Connecticut Department of Banking rules. Massachusetts caps small loans at 23 percent plus a $20 administrative fee under the state's Small Loan Statute. Illinois went further in 2021 with the Predatory Loan Prevention Act, which imposes a 36 percent all-in APR cap that includes ancillary fees.

If a lender quotes you a number above those caps and claims to be licensed in your state, something is wrong. Either the loan is structured to dodge the cap (membership fee, "tribal" affiliation, offshore incorporation) or the lender is operating without authorization.

Why Illegal Lenders Still Show Up in Your Google Results

State licensing is enforced by state regulators, not by Google. A lender chartered in Belize or operating under a tribal-government affiliation in Oklahoma can buy search ads aimed at borrowers in Manhattan. Whether that lender can legally collect on the loan in Manhattan is a separate question, and one most borrowers never get to. We cover the tribal angle in detail in our piece on tribal lenders and sovereign immunity.

The Consumer Financial Protection Bureau has gone after several of these arrangements. The CFPB's long-running case against CashCall, which used tribal affiliation to argue state usury law did not apply, was decided against the lender. Courts have generally rejected the "tribal model" when the actual lending economics flow back to non-tribal actors. That does not stop new versions of the same setup from launching every year.

If the loan you took out was made by a lender not licensed in your state, the loan may be void or unenforceable under your state's usury statute. That is a high-stakes claim and one you should not make on your own. More on what to do about that below.

The Legal Options, Ranked From Cheapest to Most Expensive

1. Credit Union Payday Alternative Loans (PALs)

This is the option most borrowers in payday-ban states never hear about, and it is the cheapest small-dollar credit a real human can get. Federal credit unions are authorized to offer two types of PALs under National Credit Union Administration rule 12 CFR 701.21.

PALs I run from $200 to $1,000, term of one to six months, maximum APR of 28 percent, application fee capped at $20. You need to have been a credit union member for at least one month. PALs II go up to $2,000, term of one to twelve months, available immediately upon joining, no rollovers, and the credit union cannot charge overdraft or NSF fees on a PAL II payment that fails. Same 28 percent APR cap.

Yes, you have to join a credit union first. No, that is not as hard as you think. Membership is usually defined by where you live, work, or worship, and the application takes about 15 minutes. Our full PAL playbook walks through the locator method and what to ask when you call.

2. A Small Installment Loan From a State-Licensed Lender

This is the lane Quick5k's lending-partner network covers, $500 to $5,000 from lenders that hold a license in the state where the borrower lives. The terms vary by state and by lender, but the loans are installment products with fixed monthly payments, not single-payment balloon notes. Because they are made by licensed lenders, the APR is subject to the state's rate cap.

For comparison, a 36 percent APR on a $1,000 six-month installment loan works out to roughly $100 in finance charges, depending on the amortization. That is more than a PAL would cost, and a lot less than the 300 percent or more an unlicensed payday lender quietly charges in the same state.

3. Earned Wage Access Through Your Employer or a Registered Provider

If your employer offers an integrated earned wage access (EWA) program, or you use a direct-to-consumer EWA app, you may be able to pull a portion of wages you have already earned before the regular pay date. EWA is legal in payday-ban states, but the legal classification of the product depends on where you live. California treats EWA as a loan under regulations finalized by the Department of Financial Protection and Innovation in October 2024. Nevada, Kansas, Missouri, Wisconsin, South Carolina, Arkansas, Indiana, Maryland, Connecticut, and Louisiana have enacted EWA-specific licensing or registration laws. Our 2026 EWA state map covers the framework in detail.

Check whether your provider is registered with your state regulator before relying on it for anything more than a one-time test. Tips and "express" fees are technically voluntary in most state frameworks but can add up to an effective cost rivaling a small installment loan if you use the service every pay period.

4. Workplace Hardship Programs and Paycheck Advances

If you work for a mid-size or larger employer, ask your HR department whether there is a hardship loan program, a paycheck advance policy, or an emergency assistance fund. These exist more often than employees realize and tend to come with zero or near-zero interest. They will not be advertised. You have to ask. See our breakdown of employer hardship grants and the EWA-versus-401k math.

5. A 0 Percent Intro Credit Card (If You Have Time)

If you have any credit and a few weeks before the money is due, a 0 percent intro APR credit card can be the cheapest tool for a one-time expense. The catch is the back-end rate, which kicks in after the promo period, typically 12 to 21 months. Run the math: if you cannot pay the balance before the promo ends, the post-promo rate will eat any savings.

A cash advance on an existing credit card is a different animal. Cash advance APRs are usually higher than purchase APRs, interest begins accruing immediately with no grace period, and there is a transaction fee. It beats a 300 percent payday loan. It loses to almost everything else on this list.

6. Buy Now, Pay Later for a Specific Essential Expense

If the money you need is for a specific essential item (a refrigerator, a car repair at a participating shop, prescription glasses), a Buy Now, Pay Later plan can split the cost into four interest-free payments. BNPL is not a cash advance, so it works only for the specific purchase. Miss a payment and the late fees stack quickly. The CFPB has been increasingly clear that BNPL providers are subject to many of the same disclosure rules as credit card issuers. Our BNPL emergency guide walks through when it is the right tool and when it is not.

7. Pawn Shop Loan or Family Loan (Honest Last Resorts)

A pawn loan trades a physical item for cash. Rates are typically 5 to 25 percent per month depending on the state, which is high, but the loan is non-recourse: lose the item and the debt is gone. No credit hit. No collection calls. If you have an item you can afford to lose, it is sometimes the right call. Our pawn-versus-installment comparison covers the math.

A family loan is the most awkward and often the cheapest. If you go this route, write the terms down. Even a one-page agreement protects both sides of the table.

Red Flags the Lender Targeting You Is Not Licensed

Some of these are obvious. Others are designed to look ordinary. Watch for:

- "Tribal" or "sovereign nation" affiliation language used as a reason state laws "do not apply."

- A website with no physical address in the United States, or an address that is a mailbox service.

- An APR that is not disclosed clearly, or that requires you to scroll through several screens to find.

- "Membership fees" or "VIP program" charges separate from the loan itself. The CFPB sued MoneyLion in 2025 for an arrangement of this kind under the Military Lending Act; the same fact pattern can also push effective rates past state caps.

- Pressure to e-sign before reading the loan agreement.

- A request for upfront fees, "insurance," or "good faith" deposits before the loan disburses. That is a classic advance-fee scam.

- Approval despite not asking for income verification, employment, or a real credit pull.

How to Look Up Whether a Lender Is Licensed Where You Live

Every state has a financial regulator and most maintain a free, searchable license database. A few to know:

- New York: search the New York Department of Financial Services license search tool at dfs.ny.gov.

- New Jersey: New Jersey Department of Banking and Insurance licensee search.

- Connecticut: Connecticut Department of Banking license verification.

- Massachusetts: Mass.gov Division of Banks licensee directory.

- Maryland: Office of the Commissioner of Financial Regulation licensee lookup.

- Pennsylvania: PA Department of Banking and Securities license verification.

- North Carolina: NC Commissioner of Banks consumer finance licensee search.

If a lender is not in the database, the lender is not licensed. That is the test, full stop. The NMLS Consumer Access site at nmlsconsumeraccess.org also offers a national lookup for many non-bank financial entities.

State-Specific Quick Notes

New York: 16 percent civil usury, 25 percent criminal usury for non-bank loans. Payday lending storefronts are not permitted. The DFS has issued multiple cease-and-desist letters to online lenders targeting New York residents.

New Jersey: 30 percent maximum APR under the Consumer Finance Licensing Act. The state Attorney General has pursued unlicensed online lenders aggressively.

Connecticut: 36 percent APR cap on small consumer loans. Check cashers cannot offer payday-style products.

Massachusetts: 23 percent plus a $20 administrative fee on small loans under the Small Loan Statute.

Maryland: Roughly 33 percent maximum APR depending on loan size under the Consumer Loan Law (verify current cap with the Office of the Commissioner of Financial Regulation before relying on a number).

Pennsylvania: The Loan Interest and Protection Law caps non-bank consumer lending at very low rates; payday lending is not a viable business model in PA.

North Carolina: The state effectively eliminated payday lending in 2006. State-chartered small installment lenders operate under capped rate tiers.

Vermont: 18 percent APR cap for licensed lenders; payday lending storefronts are not authorized.

These are pointers, not a substitute for the statute. Always confirm with the relevant state regulator's site before signing anything.

What If You Already Took a Loan From an Unlicensed Lender

First, do not stop paying on your own based on a hunch. Call your state regulator's consumer hotline, file a complaint, and ask for guidance. In several payday-ban states, loans made by an unlicensed lender are void or unenforceable, and the borrower may be entitled to recover amounts paid above principal. The exact remedy depends on the state's usury statute, the loan structure, and what court you would end up in.

Second, contact your state's legal aid office. Most consumer-protection attorneys at legal aid will at least screen the case for free, and many can take it on if the facts are strong. NACA (the National Association of Consumer Advocates) maintains a directory of consumer-rights attorneys.

Third, file with the CFPB at the CFPB complaint portal. The complaint gets forwarded to the company, the company has 15 days to respond, and the record becomes part of the CFPB database. It is not a court order, but it creates a paper trail.

One more thing: if the lender is autodialing you, texting you without consent, or calling outside the 8 a.m. to 9 p.m. window, you may have a separate claim under the Telephone Consumer Protection Act or the Fair Debt Collection Practices Act. Document the calls, save the texts, and bring that record to the attorney along with the loan documents. Our TCPA, FDCPA, and CFPB complaint playbook covers the filing mechanics.

What to Do Right Now

If you are in a payday-ban state and need short-term cash, work the list in order. Call a federal credit union about a PAL. Look into a state-licensed installment loan in the $500 to $5,000 range from a lender that holds a license in your state. Check whether your employer offers a hardship program. Ask whether your EWA app is registered with your state regulator.

If a lender approves you in seconds and you cannot find that lender in any state license database, walk away. The "approval" is the trap. The fact that they will lend to you is not evidence that the loan is legal where you live.

Frequently Asked Questions

It depends on the state. Some prohibit single-payment payday loans outright (Connecticut, New York, North Carolina). Others impose a rate cap (Illinois at 36 percent, Massachusetts at 23 percent plus a fee) that makes payday lending unprofitable as a storefront product. Check the statute or the state regulator's site to see which rule applies to you.

No. Lenders not licensed in your state can still make offers. Whether they can legally enforce the loan is a separate question, and one many unlicensed lenders are willing to bet you will not ask. Verify the license in your state's database before signing.

A PAL is a small-dollar loan offered by federal credit unions under NCUA rule 12 CFR 701.21. APR is capped at 28 percent. PALs I are $200 to $1,000; PALs II go up to $2,000. You need to be a credit union member, which usually takes a short application and a small deposit. The NCUA's MyCreditUnion.gov site has a locator.

Yes. Options include a PAL from a federal credit union, a small installment loan from a New York-licensed lender, an EWA advance from a registered provider, or a 0 percent intro credit card if your credit allows. New York's 25 percent criminal usury cap rules out a traditional payday loan, but installment credit at legal rates is available.

Do not stop paying based on your own analysis. Contact your state regulator and a legal aid attorney first. In many payday-ban states, the loan may be voidable and you may recover amounts paid above principal, but the remedy depends on state law and the loan's structure. File a CFPB complaint to create a record while you sort out next steps.

Generally yes, but the legal classification varies. California treats EWA as a loan. Nevada, Kansas, Missouri, Wisconsin, South Carolina, Arkansas, Indiana, Maryland, Connecticut, and Louisiana have EWA-specific registration or licensing laws. New York, New Jersey, and Massachusetts have not enacted EWA-specific statutes, but their existing lender licensing laws may still apply. Verify with your state regulator that your provider is registered or operating lawfully before relying on it.